We have a suite of mortgage calculators to help you work out how repayments will affect your household finances, what you could save by remortgaging, and the beneficial impact of overpaying. You can also enter your details here to see what’s available on today’s market

1 November: Stamp Duty Nil-Rate Thresholds To Fall In April

- Annual house price inflation at 2.4% in October

- Monthly increase in house prices at 0.1%

- Average UK property price is £265,738

According to the latest House Price Index from Nationwide building society, the price of a typical UK home increased by 2.4% year on year in October, down from 3.2% in September, writes Kevin Pratt.

House prices rose by 0.1% month-on-month in October.

Commenting on the figures, Robert Gardner, chief economist at the society, said: “Housing market activity has remained relatively resilient in recent months, with the number of mortgage approvals approaching the levels seen pre-pandemic, despite the significantly higher interest rate environment.

“Solid labour market conditions, with low levels of unemployment and strong income gains, even after taking account of inflation, have helped underpin a steady rise in activity and house prices since the start of the year.”

Nationwide is expecting the economy to continue to recover steadily, which it says will allow housing market activity to strengthen gradually as properties become more affordable thanks to a combination of lower interest rates and earnings outpacing house price growth.

The housing market is absorbing the fall-out from this week’s Budget, in which the Chancellor, Rachel Reeves MP, confirmed the temporary increase in nil rate stamp duty thresholds in England & Northern Ireland would expire on 31 March 2025.

For first-time buyers purchasing a property valued under £500,000, the nil rate threshold will fall to from £425,000 to £300,000. For other residential buyers, it will fall from £250,000 to £125,000.

Gardner said: “The main impact of the stamp duty changes is likely to be on the timing of property transactions, as purchasers aim to ensure their house purchases complete before the tax change takes effect.

“This will lead to a jump in transactions in the first three months of 2025, especially March, and a corresponding period of weakness in the following three to six months, as occurred in the wake of previous stamp duty changes.”

Nationwide’s analysis for the year to June 2024 suggests that the stamp duty change will affect around one in five first-time buyers, with the impact varying across the country because of the difference in house prices.

It says the most pronounced effects are likely to be in the South East of England, where 40% of first-time buyers paid between £300,000 and £425,000 for their homes.

The areas least affected are likely to be Yorkshire & The Humber, the North of England and Northern Ireland, where less than 10% of first-time buyers paid between £300,000 and £425,000 for their homes.

28 October: Property Sales Return To Peak Pandemic Levels

- Annual house price inflation at 1%

- Sales numbers at highest level since 2020

- First-time buyers most active buyer group

House prices are 1% higher than this time last year, according to September data from online property portal Zoopla, with sales activity at its highest since 2020, writes Jo Thornhill.

The number of ‘sales agreed’ is 30% higher than a year ago, with first-time buyers representing 36% of all sales, making them the largest buyer group in 2024 so far.

Zoopla says the average property price across the UK is now £267,500. It says 2024 is turning into a ‘bumper year’ for housing sales, not least because of lower mortgage costs.

Competition among lenders has seen average borrowing rates reach their lowest level in two years, while rising incomes are helping to support a higher level of sales agreed.

The portal says sales volumes are at their highest since the boom in the wake of pandemic restrictions being lifted in late 2020.

Prices are up by just 1% over the last 12 months to September 2024, compared to a moderate fall of 0.9% a year ago. Price inflation is being held back due to the relatively larger supply of properties for sale, while buying power is being kept in check by affordability pressures, says Zoopla.

Property price inflation continues to rise fastest in areas with more affordable house values, including the North East of England, where prices are up 2% annually and the average home is worth £143,400.

Prices have also risen 2% year on year in Yorkshire and Humberside, to an average value of £188,600, while prices are up by 2.3% annually in the North West to £198,100.

In Scotland average annual price inflation stands at 2.4% and a typical home is now worth £165,300, and in Northern Ireland prices are up 5.6% year on year to an average value of £176,300, according to Zoopla.

House prices are posting small falls in the southern regions of England. Average prices are down by 0.3% in Eastern England to £337,100 and prices are down by 0.1% in the South East to £388,000.

Prices are up a modest 0.6% in London, where the average home is now worth £537,400.

Responding to the data, Nathan Emerson, chief executive at estate agent trade body Propertymark, said: “We have seen an encouraging transformation across the year in terms of a resilient trend of house price growth. Affordability and overall confidence in the sector have also seen a boost throughout the year so far.

“Considering the government has an ambitious aim to deliver growth following what has been a turbulent few years, we hope that this week’s Autumn Budget will be used as a springboard to improve housing supply. Propertymark has long argued that stamp duty reform is one way to do that, especially for those wishing to downsize.

“When the Bank of England’s Monetary Policy Committee (MPC) meets on Thursday next week (7 November), we hope to see further progression on potentially cutting interest rates as this will continue to improve the overall health of the economy.”

Matt Thompson, head of sales at estate agent Chestertons, said: “The property market has been extremely active this year and we currently have 17% more properties under offer than in 2020. Pent-up demand, improved mortgage deals and people’s desire to find a property ahead of the Autumn Budget have been key motivators for house hunters to finalise their search.”

21 October: Sales Agreed Surge 29% After Weak 2023

- Average asking price up 0.3% in October

- Annual rate of price increases at 1%

- Agreed sales up 29% year-on-year

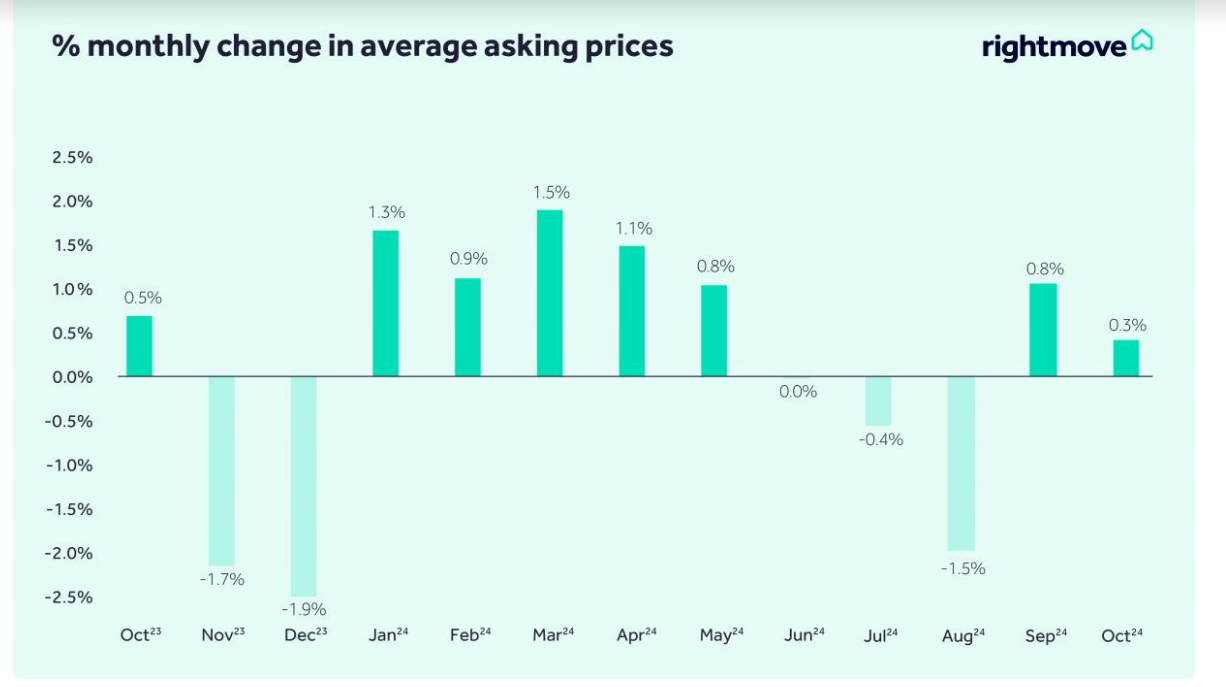

Average new seller asking prices increased by just 0.3% in October (£1,199 in real terms), according to online property website Rightmove, writes Jo Thornhill.

This is lower than the long-term seasonal average rise of 1.3% for this time of year, and means average asking prices are only 1% higher than in October 2023. The average property asking price across the country is at £371,958.

But while prices are largely flat, market activity remains strong, according to Rightmove data. The number of sales being agreed is up by 29% year-on-year, a strong rebound from the weaker market in 2023.

Underlying buyer demand remains strong, with the number of people contacting agents about homes for sale up by 17% compared with this time last year, despite uncertainty caused by what might be included in the upcoming Autumn Budget on 30 October.

The number of properties for sale is 12% higher than a year ago and is at the highest level per estate agent since 2014. But this means competition between sellers is fierce, as they look to find price-sensitive buyers.

Regionally, asking prices rose the most in London and Scotland in October. Prices were up 1.9% in Scotland to an average of £197,953, and up by 1.8% in the capital to £694,906.

On an annual basis, prices have increased the most in Scotland and the North East of England, up 5.6% and 4.9% respectively. The average asking price in the North East is now £192,742.

The South West and South East regions of England are the only areas to have seen a fall in asking prices over the past year at a drop of 0.2% and 0.6% respectively. The average asking price in the South West is now £384,237, while in the South East it stands at £483,780.

Overall, Rightmove says the market outlook is positive, but affordability pressures remain, and some buyers may be waiting for Budget clarity and cheaper mortgage rates before acting.

Tim Bannister, the portal’s director of property science, said: “This month’s subdued price growth comes as buyer choice soars to a level not seen since 2014. With the ball in the buyer’s court and the pick of a big crop to choose from, sellers need to be pricing competitively to find a buyer.

“Some sellers appear to be acting on this caution, contributing to limited price growth and better buyer affordability. This is helping to keep the number of sales being agreed consistently and strongly ahead of the [normally] quieter market of this time last year.

“Once we have more certainty about the contents of the Budget, hopefully followed by speedy second and third Bank Rate cuts, we could see another surge in market optimism like we had in the Summer. Affordability is still the biggest barrier facing many movers, with mortgage rates still high, so if the expected two cuts come to fruition it could be the boost that many buyers-in-waiting need.”

Nathan Emerson, chief executive of estate agents trade body Propertymark, said: “ Many serious buyers seem to be in the driving seat when it comes to negotiating on their next home move due to the vast choice of properties on the market. With the Bank of England’s next announcement on interest rates looming, some buyers will be cautious with their current budgets or will be waiting in the wings to see what its decision will mean for the market before moving.”

Myles Moloney, sales manager at estate agent Chase Buchanan, said: “At the beginning of October we saw continued buyer confidence which was boosted by favourable mortgage rates and a greater number of properties being put up for sale.

“As we are nearing the Autumn Budget, however, house hunters and sellers have grown more cautious. We predict market activity to pick-up after the Budget, once buyers and sellers feel that a more defined picture of the political and economic environment has been established.”

16 October: Figures Point To ‘Modestly Positive Picture’

- Average prices rise 2.8% in year to August

- Sixth consecutive month of annual increases

- Typical property now worth £293,000

Average house prices, based on data from property sales recorded by the Land Registry, rose by 1.5% in August, taking annual price inflation to 2.8%, writes Jo Thornhill.

It is the sixth consecutive month of annual increases recorded by the Office for National Statistics (ONS). The average UK house price stood at £293,000 in August, £8,000 higher than 12 months ago.

With inflation dropping to 1.7% in September, the Bank of England now looks more likely to cut its benchmark Bank Rate, currently at 5% following a cut from 5.25% on 1 August, when it next meets on 7 November.

This would provide a further boost to the property market, although increased activity could fuel house price inflation, which is bad news for first-time buyers.

Average property values increased by 2.3% annually in England to £309,572, according to the ONS. Wales has seen a 3.5% annual rise to £222,925, while prices are up by 5.4% in Scotland to £199,971.

The average house price increased in the year to the second quarter of 2024 (April to June) to £185,025 in Northern Ireland, an annual rise of 6.4%.

The latest residential property market survey published by RICS (The Royal Institution of Chartered Surveyors) shows an increase in buyer enquiries and agreed sales in August.

It says this continues to point to a ‘modestly positive picture’ for the market and house prices. The exceptions are Scotland and Northern Ireland, where house prices are rising more quickly.

Jeremy Leaf, north London estate agent and former RICS residential chairman, said: “This most comprehensive of all house-price surveys, as it includes cash and mortgage transactions, demonstrates once again considerable market strength despite reflecting activity over the past three months at a time of economic and political turbulence.

“Today’s larger-than-expected fall in inflation, added to yesterday’s wage growth, will raise expectations of further cuts in mortgage costs and be a welcome shot in the arm to buyer confidence.”

Tomer Aboody, director of specialist lender MT Finance, said: “The housing market continues to go from strength to strength with prices edging upwards as buyer and seller confidence grows. However, some of this recovery is down to the comparison with the static, slow market of last year, where prices and transactions were down.

“We are now seeing the fruits of a better economy and lower rates, with mortgages much more affordable than this time last year. Lower inflation should also persuade the Bank of England to take action and reduce rates further.”

7 October: Values Rising At Highest Pace In Two Years

- Annual house price inflation at 4.7%

- Average prices up 0.3% in September

- Mortgages agreed up 40% year on year

- Typical home worth £293,399

The average property increased in value by 0.3% in September, matching the rise seen in August, according to data from Halifax, the UK’s biggest mortgage lender, writes Jo Thornhill.

Annual house price inflation is running at 4.7%, the highest level seen since November 2022. A typical property now costs £293,399, up from £292,540 in August, following three consecutive months of price gains.

Northern Ireland continues to have the strongest annual house price growth in the UK at 9.7% in the year to September. The average property value here is now at £203,593.

Prices rose by 4.4% in Wales to an average of £224,119, and by 2.1% in Scotland to £205,718.

In England, the best performing regions are the North West, which recorded annual price inflation of 5.1% (the average home in the region is now worth £234,355) and Yorkshire and Humber, which has seen price rises at 4.3%, on average (a typical home here is now worth £210,116).

The lowest annual price increases in England were in Eastern England, at 2.3% in the year to September. The average house price in the region is £333,042.

In London, the average house price stands at £539,238, after annual price inflation was recorded at 2.6% in the year to September. But Halifax says this is still some way below the capital’s peak property price of £552,592 set in August 2022.

The average amount paid for a property by first-time buyers has increased by 4.2% over the past year. This is an extra £9,409 in cash terms and brings the typical first-time buyer property price up to £232,769, its highest level since May 2024.

However, that’s still about £1,000 less than the average amount paid by a first-time buyer two years ago (£233,760), a fall of 0.4%.

Amanda Bryden, head of mortgages at Halifax, said: “It’s essential to view these recent gains in context. While the typical property value has risen by around £13,000 over the past year, this increase is largely a recovery of the ground lost over the previous 12 months. Looking back two years, prices have increased by just 0.4% (£1,202).

“Market conditions have steadily improved over the summer and into early autumn. Mortgage affordability has been easing thanks to strong wage growth and falling interest rates. This has boosted confidence among potential buyers, with the number of mortgages agreed up over 40% in the last year and now at their highest level since July 2022.

“While improved mortgage affordability should continue to support buyer activity, boosted by expected further cuts to interest rates, housing costs remain a challenge for many. We expect property price growth over the rest of this year and into next to remain modest.”

Mark Harris of mortgage broker SPF Private Clients said: “Lenders continue to reduce their mortgage rates, which is encouraging buyers to make their move. Two-year fixes are now available from 3.84% while the cheapest five-year fix is pegged at 3.68%, which will prove to be more palatable for borrowers.

“This ongoing rate war among lenders is great news for borrowers as there are some really compelling deals being launched, which will go some way to helping affordability.”

Matt Thompson at estate agent Chestertons said: “Lower interest rates and sub-4% mortgage products saw more house-hunters start their property search in September. The uplift in buyer activity, and looming changes to capital gains tax (CGT) in the upcoming Budget, also motivated sellers to put their property up for sale.

“We expect this level of market activity to continue and could see an additional boost in buyer motivation if the Bank of England decides to cut interest rates in November.”

3 October: Lower Mortgage Rates Boost Sales By 25%

- Annual price inflation at 0.7%

- Demand up 26% as sales agreed rise 25%

- Average property price £267,100

Stable house price growth (an annual rise of 0.7% in the year to August) and the lowest mortgage rates in 15 months have boosted confidence among buyers and sellers, according to the latest house price data from Zoopla, writes Jo Thornhill.

The property portal saw a 26% increase in buyer demand in August compared to the same month in 2023.

The number of properties for sale is up 12%, with sales agreed up by 25%, compared to the same time last year. This rises to an increase of more than 25% for sales agreed in the East Midlands (32%) and in the North East of England (30%).

Zoopla says higher buy-to-let mortgage costs and speculation about tax increases on landlords in the Budget (due on 30 October) have boosted the supply of properties for sale, with landlord investors and second home owners looking to offload their properties.

The firm says 32% of homes for sale on its site are ‘chain-free’, which suggests they may be being sold by landlords.

Regionally, house prices are up over the year to August in all areas, except for the South West of England (down 0.3% to £315,400), the South East of England (down 0.2% to £338,000), and the East of England region (down 0.9% to £337,100).

The North West of England has seen the biggest annual growth in prices of all English regions at 2.1%, and the average home is now worth £198,100.

Annual house price inflation is highest across the UK in Northern Ireland, at 5.7%. The average home in the country is now worth £176,300.

Prices in Scotland are up 2.2% in the year to August, and stand at £165,300, on average, while in Wales prices have risen by 1.3% to £205,800.

The average home across the UK is now worth £267,100.

Richard Donnell at Zoopla said: “Lower mortgage rates are delivering a much needed confidence boost to homeowners, many of whom have sat on the sidelines over the last two years. Market activity is up across the board and expectations of lower borrowing costs will continue to bring buyers and sellers into the market.

“Speculation over possible tax changes in the Budget and the impact of previous tax changes are supporting the expansion in homes for sale. More supply delivers much greater choice for buyers and will keep house price inflation in check into 2025.“

Nathan Emerson at estate agent trade body Propertymark said: “We are starting to see early signs of lenders having the confidence to shift up the landscape by offering sub-4% mortgage deals, which points towards future confidence within the economy.”

Nigel Bishop of property agent Recoco Property Search said: “Second homeowners and buy-to-let investors are facing drastic changes as some local authorities have or are going to start charging double council tax for properties that are left empty for more than a year. We are seeing more second homeowners contemplating if maintaining their holiday home remains a sound financial investment.

“If a substantial number of second homes is being put up for sale, we could see the property market in areas such as Cornwall become increasingly attractive to house hunters who are seeking a permanent residence but are currently priced out of the market.

“That being said, a lot of properties are being offered at considerably high asking prices and sellers will need to adjust their expectations.”

September 30: Demand Improves As Market Continues To Settle

- Annual house price growth at 3.2%

- September figure 0.7% up on last month

- Price increases in Northern Ireland running at 8.6% (in year to Q3)

- Average home worth £266,094

House prices are rising at their fastest pace since November 2022, according to the latest data from mutual mortgage lender Nationwide building society, writes Jo Thornhill.

It recorded a 3.2% annual price rise across the country in September, up from the 2.4% the lender posted in August. This compares to an annual rise of 4.4% in November 2022.

Following a 0.7% monthly increase in September, average house prices are now only 2% below the record highs recorded in the summer of 2022.

Most regions saw a pick up in the third quarter of the year (July to September). Northern Ireland saw the biggest jump in prices, recording an 8.6% increase in the year to the end of the third quarter. The average house price in the country is now at £197,196.

Scotland also saw significant annual price increases at 4.3% taking the average price to £184,471, while prices in Wales recorded an annual rise of 2.5% to £207,113.

Prices in England are up 1.9% year on year, with the national average now standing at £304.049. London is the best performing region in the south of England, with price rises of 2% in the year to September. The average property in the capital is now worth £524,685.

East Anglia was the only UK region to record a fall in annual prices, showing a decline of 0.8% compared to last September. The average home in the region is now at £270,906.

Robert Gardner, chief economist at Nationwide said: “Income growth has continued to outstrip house price growth in recent months, while borrowing costs have edged lower amid expectations that the Bank of England will continue to lower interest rates in the coming quarters.

“These trends have helped to improve affordability for prospective buyers and underpinned a modest increase in activity and house prices, though both remain subdued by historic standards.”

Estate agent and former RICS chairman Jeremy Leaf said: “The market has changed and demand is improving which has coincided with lower mortgage rates and a more settled picture for inflation and politics.

“This shift has resulted in more appraisals, listings, offers and firming pricing. But with the choice of properties and mortgages rising, a fear of missing out is also prevailing. Uncertainty remains an obstacle, particularly at the higher end, probably at least until after the Budget at the end of October.”

Sarah Coles, head of personal finance, Hargreaves Lansdown added: “While it was great news for sellers who need a buoyant property market to shift their home, it’s less positive news for first-time buyers, who can see the property of their dreams move even further out of reach”.

The latest mortgage data from the Bank of England’s Money and Credit report has also found that net mortgage approvals for house purchase increased to a two-year high, rising from 62,500 in July to 64,900 in August. It is the highest level since August 2022, when approvals for purchase were recorded at 72,000.

Approvals for remortgaging have also increased from 25,200 in July to 27,200 in August.

Overall, individuals borrowed a net £2.9 billion in mortgage debt in August, up slightly from £2.8 billion in July, reflecting continued demand for housing.

Rosie Hooper, chartered financial planner at Quilter Cheviot, said: “The Bank of England’s statistics for August, combined with this morning’s house price growth figures from Nationwide, paint a picture of a housing market that is regaining momentum amid easing borrowing costs and renewed buyer activity.

“The mortgage approval rise indicates that prospective buyers are taking advantage of improving market conditions and lower mortgage rates and locking in more favourable deals.”

18 September: Average House Prices Up 2.2% As Market Steadies – ONS

- Fifth consecutive month of annual increases

- Average home now worth £290,000

Annual house price inflation is running at 2.2% in the year to July, according to the latest data released by the Office for National Statistics (ONS), writes Jo Thornhill.

It’s a slight fall from the 2.7% annual increase recorded in the year to June. But it marked the fifth consecutive month of price rises, indicating continued stability in the market. Previously there had been eight consecutive months of annual price falls.

The monthly increase to house prices was a nominal 0.6% and takes the value of the average home across the country to £290,000.

The ONS index, which uses Land Registry data on sold properties, shows variations in the countries and regions.

The average house price in England is up by 1.6% annually and the average value of a home is now at £305,879.

In Wales prices rose 2% in the year to July to stand at an average value of £218,184, while prices in Scotland are up by 6% to £199,398 over the same time period.

Average prices increased in Northern Ireland by 6.4% in the year to the end of June 2024 (end of the second quarter of the year). It is the biggest annual change of any region and takes the value of a typical home in the country to £185,025.

Mark Harris, chief executive at mortgage broker SPF Private Clients, said: “With inflation sticking at 2.2% and expected to edge up in the autumn, it’s unlikely this will trigger a further rate cut from the Bank of England this month, although the markets still expect at least one further rate reduction before the end of the year.

“The good news for borrowers is that mortgage rates continue to soften, with Santander introducing a sub-4% two-year fix on the back of the lowest two-year Swap rates in two years. There are also plenty of five-year fixes at sub-4% for those looking for certainty over a longer period.

“While rock-bottom rates have long gone, these reductions are giving borrowers some comfort after a prolonged period of rising rates. Competition between lenders is likely to mean further gentle reductions in mortgage rates as they vie for new business.”

Amy Reynolds, head of sales at Richmond estate agency Antony Roberts, said that most properties are getting a good number of viewings but realistic pricing remains paramount.

She said: “This isn’t a market where buyers are coming in with big offers, there are some exceptions to this but most people want to see properties that are reasonably priced and not waste their time. In a rising market, you can ask a high price and know applicants will view and offer but a flat market is very different.

“It looks unlikely that the Bank of England will cut rates this month but a November rate cut, while too late to impact the housing market this year, will help kickstart the 2025 market.”

16 September: Buyers Return To Market Encouraged Cheaper Mortgages

- Average asking prices up 0.8% in September

- Annual price growth running at 1.2%

- Number of sales agreed up 27%

The average asking price of property coming on to the market is up 0.8% in September compared to August, according to the UK’s largest property portal, Rightmove. With annual inflation at 1.2%, it takes the average seller price across all property types to £370,759, writes Jo Thornhill.

Rightmove says it is usual to see a monthly rise in prices in September, but this year’s 0.8% increase is double the long-term average rise, with stable prices supported by increased market activity.

Buyers and movers are likely to have been buoyed by the August cut to interest rates by the Bank of England to 5% from 5.25%, with the potential for further cuts at the next decision meeting this Thursday (19 September), or in November.

The number of sales being agreed is up by 27% year on year, a strong rebound compared with last year’s more subdued market. Rightmove says this is most likely due to a release of pent-up buyer demand.

Homeowners also appear more confident to come to market, with the number of new sellers listing homes for sale up by 14% compared to this time last year.

The average number of available properties for sale per estate agent is 33 – marking its highest level since 2014. This has come from a 14% increase in new properties coming to the market for sale compared with last year. But homes ae still in relatively limited supply, says Rightmove, as this figure is only up by 3% when compared with the more usual pre-pandemic 2019 market.

Despite some encouraging signs from the market, estate agents report buyers are still cautious and particularly price-sensitive. The average property seller is taking 60 days to find a buyer – three days longer than at this time last year despite better market conditions and lower mortgage rates.

Tim Bannister, Rightmove’s director of property science, commented: “The Autumn action has started early with a strong rebound in activity from both buyers and sellers compared to the subdued market at this time last year, continuing the momentum from the better-than-expected summer market.

“The certainty of a new government followed by the first Bank Rate cut in four years invigorated the market, opening a window of opportunity for movers to act. Some of this will be pent-up demand from those who had to hit the pause button until now.”

He added: “However, windows of opportunity tend to need a momentum of good news to stay open, and there are still uncertainties ahead which could cause some of the current market activity to ease.”

On a regional basis, average asking prices are up in September, both monthly and year-on-year, in all areas with two exceptions; the East of England, where prices fell 0.3% and are flat (0%) annually, and in the South West of England where prices are down 0.8% (although they are up 1% year on year).

The average asking price in the East of England is now at £418,110, and at £387,389 in the South West.

Average asking prices increased the most in September in Scotland and the West Midlands, both up by 1.1%. The average home for sale is at £194,180 in Scotland and at £293,796 in the West Midlands.

Annually, asking prices have risen the most in the North East of England, according to Rightmove, up by 5% year on year to stand at £193,706.

Nathan Emerson, chief executive at estate agent trade body Propertymark, said: “It is positive news to see further uplift across the housing market now affordability has more confidently swung in the direction of consumers.

“We are keen to see further dips in the Bank of England Bank Rate as conditions permit, but at this point it is important to consider what effect the Budget at the end of next month may have on the housing market and if today’s figures reflect a keenness by consumers to complete on a property before any potential changes to the current tax structure might be announced.”

Tony Gambrill, regional sales director at London-based estate agency Chestertons, said: “Due to pent-up demand from buyers, London’s property market was experiencing an unusually busy summer whereby sellers still had the upper hand during price negotiations.

“House hunters felt that market conditions had improved amid lower mortgage rates and were keen to finalise their search. This additional buyer confidence will result in demand remaining high well into the autumn.”

6 September: Annual Price Growth Strongest Since 2022

- Average prices up 0.3% in August

- Annual increase running at 4.3%

- Typical property stands at £292,505

Annual house price inflation is at its highest level since November 2022, according to the latest data from mortgage lender Halifax, after values were recorded to be increasing at 4.3% in the year to August.

The monthly increase in average prices for August was 0.3%, down from the 0.9% rise recorded in July.

The average home across the UK is now worth £292,505.

Northern Ireland has the strongest property price growth of any region. Prices rose by 9.8% to reach £201,043 in the year to August, according to Halifax.

Wales also recorded strong growth, with prices up by 5.5% annually to £224,043.

Scotland has seen more modest growth in prices over the past year. The average home is now worth £205,144, which is 1.7% higher than a year ago.

The North West of England has seen the strongest price growth in the year to August of any English region. Prices are up 4% to an average of £232,917. While Eastern England had the weakest annual price growth at just 0.3%. Average prices stand at £330,511.

London has the most expensive property prices in the UK at an average of £536,056, which is an annual increase of 1.5%

Amanda Bryden, Halifax’s head of mortgages, said: “Annual price growth has risen at the strongest rate since November 2022, but this is due in large part to the comparison with weaker growth this time last year.

“Recent price rises build on a largely positive summer for the UK housing market. Prospective homebuyers are feeling more confident thanks to easing interest rates. Such has been the resilience of house prices that the average property is now just £1,000 shy of the record high set in June 2022 (£293,507).

“While this is welcome news for existing homeowners, affordability remains a significant challenge for many potential buyers still adjusting to higher mortgage costs.

“With market activity picking up and the possibility of further interest rate reductions to come, we expect house prices to continue their modest growth through the remainder of this year.”

Karen Noye, mortgage expert at Quilter, said: “A dip in activity is usually to be expected in the summer months, but this year it appears to be minimal, and we are instead seeing signs of an ongoing recovery in the housing market. Though the report from Halifax is somewhat at odds with others, such as Nationwide which reported a fall in prices in August (see story below), there remains a general consensus that growth, at least on an annual basis, is picking up speed.

“The Bank of England’s decision to cut its base rate from 5.25% to 5% at its most recent monetary policy meeting (in August) will no doubt have contributed to the relatively robust market we have seen this summer, and as conditions become more predictable, we could see a rebound in prices in the autumn.”

The next Bank of England Bank Rate decision is due on 19 September.

Mark Harris at mortgage broker SPF Private Clients said: “The mortgage environment remains volatile, with lenders pulling deals and repricing at short notice. However, unlike a few months ago, the difference now is that mortgage rates are falling rather than rising, which is good news for affordability. Mortgage rates are at their lowest levels since March.

“As rates have fallen, we have seen activity noticeably increase. Estate agents report that August was busy as motivated movers who may have delayed for a while have got on with their transactions, while we have seen people take advantage of more palatable rates.”

30 August: Easing Of Mortgage Costs Gives Market A Boost

- Annual growth at 2.4% in August

- Prices edge down 0.2% month-on-month

- Average cost of a home in August at £265,375

Monthly house prices nudged downwards by 0.2% in August to an average £265,375 (from £266,334 in July), but a strong annual rate of growth is indicating a resilient market, writes Laura Howard.

The average cost of a UK home in August was 2.4% higher than a year ago, according to Nationwide’s latest house price report. It’s a slight increase on the 2.1% recorded in July and marks the fastest pace of growth since December 2022 when the figure was at 2.8%.

Robert Gardner, chief economist at Nationwide commented: “While house price growth and activity remain subdued by historic standards, they nevertheless present a picture of resilience in the context of the higher interest rate environment and where house prices remain high relative to average earnings which makes raising a deposit more challenging.”

He added: “Providing the economy continues to recover steadily, as we expect, housing market activity is likely to strengthen gradually as affordability constraints ease through a combination of modestly lower interest rates and earnings outpacing house price growth.”

Lenders have been pegging down the cost of mortgage deals for the last few weeks, both in the lead-up and following the Bank of England cutting interest rates from 5.25% to 5% on 1 August. The next decision by the Bank’s rate-setting monetary policy committee is on 19 September with expert opinion divided on whether a further cut will be made.

Alice Haine, personal finance analyst at Bestinvest by Evelyn Partners, said: “With more sub-4% mortgage rates now available and the prospect of more interest rate cuts this year, buyers are flooding back into the market as improving affordability levels raise the likelihood that people can net their desired home.”

Mark Harris, chief executive of mortgage broker SPF Private Clients, added that, “while the days of rock-bottom mortgages may be long gone, a more palatable pricing is helping sentiment.”

Energy-efficiency having greater effect on property values

Nationwide’s data also looked at the extent to which the energy efficiency of a property can affect its value by including ratings from energy performance certificates (EPCs) on owner-occupied homes in its house price calculations. It found that a more energy efficient property (rated A or B) attracted a modest premium of 2.8% compared to a similar home with the most common D rating. There was little difference for properties rated C or E compared with D.

The effect of the EPC was most noticeable on properties rated F or G (the lowest energy efficiency ratings) which were valued at 4.2% lower than a similar D rated property, on average (see chart below).

Nationwide’s Robert Gardner said: “Our research suggests while energy efficiency impacts remain relatively modest, they have increased relative to pre-pandemic levels, with A/B properties now attracting a larger premium compared with 2019 and F/G properties seeing a larger discount.

“Decarbonising and adapting the UK’s housing stock remains critical if the UK is to meet its 2050 emissions targets, especially given that emissions from residential buildings account for 15% of the country’s greenhouse gas emissions.”

28 August: Buyers Remain ‘Price Sensitive’ As Annual Prices Nudge Up Just 0.5%

- Annual price inflation at 0.5% in July

- House prices rise 1.4% in first seven months of 2024

- Typical home in July worth £266,400

House price inflation remains subdued, according to the latest figures from online property portal Zoopla, with average prices in July just 0.5% higher than last year, writes Jo Thornhill.

The average home last month was worth £266,400, a nominal increase on the £265,600 average figure recorded by Zoopla in June.

But Zoopla’s experts report that market conditions are continuing to improve. The last seven months showed a bigger rise in average prices of 1.4%, when compared to the rise over the last 12 months.

The property portal also recorded a 20% increase in buyer demand in the four weeks to 18 August, compared to the same period in 2023, and a 23% increase in the number of agreed sales.

It said that estate agents are listing an average of 33 homes for sale in August, the highest level since 2017.

The long-awaited cut in interest rates by the Bank of England on 1 August was welcome news for borrowers. However, Zoopla says the five-fold increased in demand is due to the large drop in demand during summer of 2023, rather than cheaper borrowing.

Potential buyers remain highly price sensitive. One in five properties (20%) listed on the market in August has undergone reduction to the asking price by 5% or more, an above-average level, according to Zoopla. Although it is below the record high of 23% seen in Autumn 2023.

Properties that require an asking price cut take more than twice as long to sell as homes without asking price changes.

Zoopla’s data shows the average time to find a buyer for homes that have no need for a price reduction is 28 days, for example, compared to 73 days for properties which have had at least a 5% cut to their original asking price.

Of the 20 cities across the country where Zoopla collects asking price data, Belfast has seen the biggest price rises in the year to July 2024 at 5.1%. The average home in the city is now on the market at £176,700.

Prices in Manchester, Liverpool and Glasgow have also held up relatively well, rising by 2%, 1.7% and 1.6% respectively. Average asking prices in July were £226,600 in Manchester, £159,600 in Liverpool and £149,400 in Glasgow.

Among the biggest annual price falls, the average asking price of a home is £136,100 in Aberdeen, which has seen average reductions of 2.5%. Portsmouth has seen annual falls of 1.1% taking the typical asking price to £279,100.

Average asking prices in London remain the highest across the country at £536,300, a nominal annual rise of 0.2%.

Richard Donnell, executive director at Zoopla said: “Momentum in the sales market continues to build as mortgage rates drift lower and more sellers gain the confidence to list their home for sale. Buyers have much greater choice which will support sales numbers, but this will keep prices rises in check.

“Buyers have less purchasing power than two or three years ago and remain price sensitive. This means sellers can’t afford to get ahead of themselves on where to set the right price for their home. If you need to cut the asking price by 5% or more then your home will take twice as long to sell or may not sell at all”.

Nathan Emerson, chief executive of Propertymark, the trade body for estate agents, said: “There is a real positivity within the housing market now that the economy seems to have stabilised.

“This is the Government’s chance to take advantage of current market confidence by clarifying a more precise time-frame for its target of building nearly two million new homes across the next parliamentary term.”

19 August: Portal Predicts 1% Annual Increase In Values

- Average asking prices drop 1.5% in August

- Bank Rate cut boosts market activity

- Average Rightmove price £367,785

The average asking price of properties coming on to the market fell by 1.5% month-on-month in August, taking annual price inflation to a nominal 0.8%, according to online property portal Rightmove, writes Jo Thornhill.

The drop in new seller asking prices, equivalent to a fall of £5,708 in real terms, takes the average price nationally to £367,785.

Rightmove says this type of drop is usual for the summer months. August has seen a monthly decline in prices from July for the last 18 years, according to its data.

The portal says that market activity has gone up due largely to the cut in interest rates by the Bank of England, which reduced the Bank Rate from 5.25% to 5% on 1 August, boosting buyer and seller confidence.

Rightmove reports a 19% jump in the number of potential buyers contacting estate agents since 1 August, compared to the same period in 2023. This compares to an 11% increase seen in July this year. The number of new sellers putting their homes on the market is up 5% compared to this time last year.

Rightmove has subsequently raised its forecast for house price inflation for 2024 from a drop of 1% to an increase of 1% for the year.

Tim Bannister, Rightmove’s director of property science, said: “The first Bank Rate cut since 2020 has sparked a welcome late summer boost in buyer activity.

“While mortgage rates aren’t yet substantially lower since the rate cut, the fact that the long-hoped-for first cut has finally arrived, and mortgage rates are heading downwards, is positive for home-mover sentiment. As the summer holiday season comes to an end, the conditions are there for a more active autumn market.”

Regionally asking prices fell in August in all areas, except Yorkshire and Humberside, where average asking prices rose by a nominal 0.3%. Yorkshire has seen annual price rises of 3.5% and the average asking price is £252,835.

Despite this month’s regional price falls, over the year to August prices have risen in every region except the East of England, South West and the South East of England.

The East of England has seen an annual price drop of 1.4%, where the average asking price is £418,295. In the South West average seller prices are down by 2.4% and the average price is now at £383,416, and in the South East, prices are down by 1.2% year on year and the average price is £480,108.

In London asking prices were up by 0.7% in August, although year on year they are down by 2.1% to an average of £677,794.

Jeremy Leaf, north London estate agent, said: “There is no doubt the cut in Bank Rate has been a shot in the arm for the housing market, particularly in terms of new enquiries during the traditionally quiet summer period.

“However, the change was anticipated for such a long time so helped soften mortgage pricing on the high street. This meant the impact on property values has been modest to date. Of course, Rightmove’s asking prices are not selling prices but do reflect an important trend in seller aspiration and confidence.

“With so many buyers, sellers and others involved in the transaction process now on holiday, obtaining commitment to proceed has been tricky although we certainly expect momentum will return from early September.”

Matt Thompson, head of sales at estate agent Chestertons, said: “Despite the summer holidays, we are currently seeing more house hunters starting or resuming their search than we did in August of last year.

“This increase in buyer activity is predominantly driven by lower interest rates and the availability of more attractive mortgage products which is even tempting first-time buyers to take the first step towards home ownership.”

14 August: Market Buoyed By Cheaper Mortgage Costs

- UK house prices rise 2.7% in year to June

- Monthly rise for June recorded at 0.5%

- Average home worth £288,000

Average property values increased by 2.7% in the year to June, according to the latest figures from the Office for National Statistics (ONS), writes Jo Thornhill.

On a monthly basis, the data shows prices were almost flat, at just 0.5% higher in June compared to May. However, it’s the fourth consecutive monthly rise, following eight previous months of annual price falls.

It takes the average property value in the UK to £288,000.

The ONS index, which uses Land Registry data on sold properties, shows variations in the countries and regions. The average house price in England is up by 2.4% annually and the average value of a home is now at £305,000.

In contrast prices were up by 4.3% in Scotland, where the average property value is now £192,000. Wales saw more modest annual price growth at 1.8% The average property price in the country now stands at £216,000.

Northern Ireland has shown the biggest annual increase, with a rise of 6.4% in the year to the end of the second quarter of 2024 (to the end of June 2024). Average property prices in the country stand at £185,000.

Among the English regions, annual house price inflation was highest in Yorkshire and the Humber, where average values increased by 4.7% in the 12 months to June. The average home in the region is now worth £215,347.

London, which is home to the highest average property values at £523,134, recorded the lowest annual price inflation of any region at just 1.2%.

Source: ONS, July 2024

Larger homes, including terraced houses, semi-detached and detached properties have seen the biggest annual house price increases compared to flats and maisonettes, according to the ONS data.

The average semi-detached house has risen by 4% in the year to June, for example, from £269,998 to £280,895.

Source: ONS, July 2024

Commenting on the ONS figures, Jeremy Leaf, estate agent and a former RICS residential chairman, said: “Here’s another example of the housing market’s resilience – very little change in prices at a time of considerable election and interest rate uncertainty. Activity has improved since, helped by the long-awaited cut in interest rates.”

Mobeen Akram, new homes director at mortgage broker the Mortgage Advice Bureau, said: “This latest house price data, coupled with the recent reduction in interest rates, is certainly a welcome relief for those who have been waiting for positive change in the housing market.

“Though the Bank Rate reduction to 5% is good news, we may still experience a slow market over the next while, as we move through the natural summer lull.”

Mark Harris, chief executive of mortgage broker SPF Private Clients, said: “With inflation rising by less than expected, this shouldn’t negatively impact the Bank of England’s plan for reducing interest rates, with the markets pricing in a further two rate reductions this year.

“The first rate cut since the pandemic has been well received and sends out an important message that rates have peaked and are on a downward trajectory. How fast those further rate reductions come will depend on the state of the economy and inflationary pressures.”

Lenders have been reducing their mortgage costs in recent days, with Barclays and Nationwide now offering the cheapest five-year fixes from 3.83%.

7 August: Bank Predicts Further Growth As Rate Cuts Begin

- Average values up 2.3% year-on-year

- House prices up 0.8% in July

- Average property price £291,268

House prices jumped up last month, taking the annual rate of price inflation in the year to July to 2.3%, according to the latest figures from Halifax, writes Bethany Garner.

This annual rate of change is a notable upswing from the 1.6% recorded for three consecutive months between April and June.

Recent cuts in mortgages rates, including some five-year fixed-rate offers below 4%, seem likely to encourage further housing market activity,

As in June, Northern Ireland saw the strongest growth in house prices. Properties in the region rose in value by 5.8% on average in the year to July – up from 4.1% the previous month. The average property in Northern Ireland now costs £195,681.

The North West of England also recorded strong growth, with the average property price rising 4.1% in the year to July, to £232,489.

In Wales, average prices rose 3.4% year-on-year, to £221,102. This marks the largest annual price rise Halifax has recorded in the region since October 2022.

Scotland also saw average prices increase, rising 2.1% to £205,264 in the year to July.

Only one UK region experienced a year-on-year decrease in average house prices – Eastern England. Properties in the region are now worth £330,282 on average, down 0.4% on an annual basis.

Homes in London continue to be more expensive than any other UK region. As of July, the average price for a home in the capital was £536,052, up 1.2% compared with July 2023.

Amanda Bryden, head of mortgages at Halifax, said: “Against the backdrop of lower mortgage rates and potential further Bank Rate reductions, we expect house prices to continue a modest upward trend throughout the remainder of this year.”

Holly Tomlinson, financial planner at Quilter, said: “Prospective buyers are now faced with a dilemma about whether to fix their mortgage now or wait for rates to come down further.

“Lots of clients in the midst of remortgaging or buying are considering tracker mortgages without early repayment charges, allowing them to benefit from future rate cuts with the option to fix when rates are lower.”

Iain McKenzie, chief executive officer of the Guild of Property Professionals, said: “The recent Bank of England rate cut and reductions in mortgage rates are positive developments for the market.

“These factors should help improve affordability for many potential buyers, especially first-time buyers who have been struggling to get onto the property ladder. However, we must acknowledge that affordability constraints and limited housing stock continue to pose challenges.”

1 August: Market ‘Holding Steady’ Ahead Of Potential Rate Cut

- House prices up 0.3% in July

- Annual rise stands at 2.1%

- Average property price £266,334

Average property prices grew by a marginal 0.3% in July, according to the latest figures from Nationwide building society, writes Jo Thornhill.

The annual rate of price growth has picked up from 1.5% in May to 2.1% for July, taking the average home to a value of £266,334 and showing modest recovery in the market.

Robert Gardner, chief economist at Nationwide, said: “The slight pickup in the annual rate of house price growth from 1.5% in June, to 2.1% in July is the fastest pace seen since December 2022. However, prices are still around 2.8% below the all-time highs recorded in the summer of 2022.

“Housing market activity has been holding steady in recent months with the number of mortgages approved for house purchase at around 60,000 per month. While this is around 10% below the level prevailing before the pandemic, it is still a respectable pace given the higher interest rate environment.”

Gardner points to the fact that affordability is still stretched for many prospective buyers. For borrowers with a 25% deposit, the rate on a five-year fixed rate mortgage deal has been around 4.6% in recent months. This is more than double the 1.9% average recorded in 2019.

Nationwide says that for first-time buyers the monthly mortgage payment is typically equivalent to around 37% of take-home pay, well above the 28% average prevailing pre-Covid and the long-run average of 30%.

The Bank of England’s Monetary Policy Committee (MPC), which decides on interest rates, is due to meet at noon today (1 August).

A reduction to the Bank Rate, currently at 5.25%, would be welcomed by cash-strapped homeowners and potential house buyers.

But with the US Federal Reserve leaving US interest rates on hold yesterday (it voted to keep rates at the target range of 5.25% to 5.5%, a 23-year high), most experts are predicting the Bank of England will follow suit. That means the next rate cut is now more likely to be in September.

Amy Reynolds, head of sales at Richmond-based estate agency Antony Roberts, said: “Hot, sunny weather, combined with buyers, who may have delayed their plans, now wanting to get on with their house moves is resulting in a busy time for the housing market.

“In our offices, we are hearing increased talk about the prospect of interest rates falling, with vendors hoping and buyers wishing that this will happen imminently.

“However, buyers need to be careful what they wish for as cheaper mortgages will almost certainly mean higher asking prices. If we see a flurry of new applicants coming back to the market, encouraged by cheaper mortgage rates, then these higher prices are likely to be achieved.”

Nathan Emerson, chief executive at estate agency trade body Propertymark, said: “The housing market is regaining a real sense of positivity. Now that inflation appears to be staying within target it would further stimulate growth within the housing sector if the Bank of England feels confident enough to allow a slight interest rate cut when the Monetary Policy Committee meets later today.

“It has been widely anticipated that they may look to lower the Bank Rate, and at a time when we have a new government who have committed to building two million new homes by 2029, this combination of factors could lead to a rejuvenation for the housing sector.”

30 July: Sellers In June Achieve Almost Full Asking Price

- House prices flatline rising just 0.1% in the year to June

- Supply of homes for sale up 16%

- Buyers pay 96.8% of asking prices

House price inflation has stalled, according to the latest data from online property portal Zoopla – but market activity is picking up, writes Jo Thornhill.

Average prices nudged up by 0.1% in the year to June, which equates to just £310 in real terms, according to the latest data from Zoopla. It puts the average UK house price at £265,600.

The data also shows significant regional variations in house price movement with annual falls of 1.2% in the East of England region (where typical values are £336,300), to an annual rise of 3.9% in Northern Ireland (where average prices are £172,550).

Prices in Wales are up 1.1% annually with the average home in the country now worth £204,700. Prices in Scotland increased 1.4% year-on-year putting the average cost of a home at £163,900.

In London average prices have fallen by 0.3% year-on-year. The cost of a typical home in the capital is now £536,500, according to Zoopla.

But while Zoopla’s experts say the housing market is continuing to adjust to higher mortgage rates with a softening of prices, it is seeing evidence of increased activity.

It reports there are 16% more properties for sale than at this time last year, and properties are achieving, on average, 96.8% of the asking price.

Other indicators also show the market is operating back at pre-pandemic levels, says Zoopla. Buyer demand was up by 20% in the four weeks leading up 21 July, compared to same four weeks across 2017, 2018 and 2019, as the following graphic demonstrates:

The Bank of England’s Monetary Policy Committee (MPC), which sets interest rates, is due to this Thursday (1 August).

But market experts are predicting that the MPC will keep the Bank Rate, currently at 5.25%, on hold this month while it checks that inflation has stabilised. Most pundits now believe the first reduction to the Bank Rate will be in September.

Richard Donnell, executive director of research at Zoopla, said: “The outlook for the housing market continues to improve with more sales, and buyers paying a greater proportion of the asking price. The first cut to the Bank of England Bank Rate will boost market sentiment and market activity over the second half of the year.”

Gary Howorth, sales director at estate agent Chestertons, said: “Although there is still some uncertainty over the Bank of England’s decision to cut interest rates this week, we have seen an uplift in the number of buyers making an offer in July. The return of buyer confidence has been further boosted by some lenders introducing more beneficial mortgage products, including deals at sub 4% interest rates.

“As many considered the result of the general election forgone and with Labour suggesting an increase in capital gains tax, we also saw more homeowners wanting to sell, contributing to an overall busier than usual month in July.”

- House prices in Wales have risen for the first time in more than a year, according to separate data from Principality building society. The mutual lender’s figures show average property values rose by 3.1% in the second quarter of 2024 (April to June) to £236,369. It follows five consecutive quarters of house price falls in Wales.

However, prices are still down 2.4%, compared to this time in 2023, and are 5% below their peak of £249,000 recorded at the end of 2022.

17 July: Average Values Up 2.2% In The Year To May

- Property values rise 1.2% in May

- House prices grow by 2.2% annually

- Average price reaches £285,201

The average home rose in value by 2.2% in the 12 months to May, according to the latest government data from the Office for National Statistics (ONS), writes Jo Thornhill.

On a monthly basis, prices were 1.2% higher in May compared to April, found the ONS which uses Land Registry data on sold properties (see our house price indices guide for an explanation of the different measures).

It takes the average property price across the country to £285,201.

Among English regions, annual house price inflation was highest in Yorkshire and the Humber, where average values increased by 3.9% in the 12 months to May 2024. The average home in the region is now worth £209,055.

London, which has the highest average property values at £523,376, recorded the lowest annual inflation. Prices increased by a nominal 0.2% in the capital in the 12 months to May.

Northern Ireland has seen house price inflation of 4.0% over the 12 months to Quarter 1 (January to March) 2024. The average home is now worth £178,499.

In Wales average prices have risen by 2.4% to £216,002 in the year to May, and in Scotland prices rose by 2.5% to £191,435 over the same period.

Larger sized homes, such as second-stepper and top-of-chain homes, have fared strongest in terms of price growth over the past year. Detached homes values have increased on average by 3.5%, while semi-detached have grown by 3.9%.

Smaller properties and the traditional first-time buyer market of flats and maisonettes have seen a drop of 0.9% in average price over the year to May, as the chart below shows.

Source: ONS, July 2024

Tomer Aboody, director of specialist lender MT Finance, said: “The continued steady growth in property values demonstrates a confidence among buyers and sellers to commit to their moves, even though rock-bottom interest rates are a thing of the past.

“As always, we would like to see more transactions. Hopefully, some interest rate cuts in the near future will help push the market on.”

Jeremy Leaf, north London estate agent and a former RICS residential chairman, said: “Though the figures are a little historic, this is the most comprehensive of all the housing surveys as it includes the (approximate) 40% of properties bought without mortgages, and has proved a reliable indicator of market health.

“The figures reflect the period in particular before the announcement of the election, but that event put the brakes on activity for some as it created considerable uncertainty. Many will hope today’s announcement of inflation holding steady (at 2%) and on target will hasten the albeit small likely drop in Bank of England Bank Rate next month, which is of more relevance to decision-making.”

Sara Palmer, a director at specialist lender, The Mortgage Lender (TML), said: “A consistent increase in house price growth this year suggests a growth in consumer confidence.

“The recent cuts in mortgage rates by leading high street lenders provide a sense of security for prospective buyers, especially with a potentially reduced interest rate by the Bank of England to come later this summer, helping to drive demand.”

15 July: Market Holds Breath As Bank Rate Decision Looms

- July asking prices dip 0.4%

- Prices up 0.4% annually

- Sales agreed up 15% year-on-year

- Average price £373,493

The average asking price of property coming onto the market fell by 0.4% in July, (£1,617 in cash terms), according to online property site Rightmove, down on the long-term average for July of falls of 0.2%, writes Jo Thornhill.

Asking prices have been largely static over the past 12 months, rising 0.4% in the year to July, as the market has been affected by higher mortgage costs. The average asking price across the country now stands at £373,493.

Rightmove says market activity was broadly steady during the general election campaign. It says there is evidence many potential buyers and movers are waiting for the first cut in interest rates by the Bank of England (its next meeting is on 1 August), while some are continuing with their moving plans.

The number of sales agreed is 15% higher than the same period a year ago, when mortgage rates were approaching the peak. The Bank of England Bank Rate, the benchmark interest rate, has been at a 16-year high of 5.25% since August last year.

Buyer demand remains stable, although there has been a drop in demand of 2% in the first-time buyer sector, where buyers are likely to be most rate and price sensitive.

Regionally, asking prices have risen, albeit marginally, over the past year in most areas, but particularly in the north of England and Scotland, where average property prices tend to be lower than the Midlands and South of England.

Average asking prices are up by 1.7% in Scotland, year on year (average asking price is now £195,344), by 4.6% in the North East of England (£193.043) and by 3.5% in the North West of England (£264,256). Prices are also up annually in Wales by 1.9%, where average asking prices are now £265,679).

In contrast, prices have fallen over the past year, by 1% in the South West of England (average asking price is £392,961), by 0.9% in the South East (£485,733) and by 0.4% in the East of England (£424,262).

While asking prices fell by 0.4% in July in London, asking prices are up over the past 12 months by a marginal 0.6%. Experts report prices have been largely flat in the capital. The average asking price stands at £692,544.

Tim Bannister, Rightmove’s director of property science, said: “A key concern for many home movers is when the first Bank of England rate cut will be, and there are signs that some pockets of movers are waiting for this before acting. Overall buyer demand, measured by the number of would-be buyers contacting estate agents about homes for sale, has remained stable in the last four weeks when compared with this time last year.

“An interest rate cut is expected to lead to lower mortgage rates, which could be the gamechanger for some would-be movers who are being held back by significantly higher monthly mortgage costs.”

Matt Nicol, managing director at estate agent Nicol & Co, in Worcestershire, said: “We have seen a positive first half in 2024, with the market feeling reminiscent of pre-Covid times, which continued despite the prominent issues of Brexit and the general election.

We’re experiencing healthy supply and demand levels, but the lack of mid-market homes has meant that first-time sellers are finding their options limited.

“Despite this, valuations and instructions remain strong, backing up the historical data that shows elections have minimal market impact. With inflation down to 2% and potential interest rate reductions ahead, the outlook remains optimistic.”

Nathan Emerson, chief executive at trade body Propertymark, said: “Any slight dip in house prices is likely to only be a temporary phase following a period of uncertainty triggered by the recent general election. Once we start to hear more news from the new government about how they intend to build 1.5 million new homes before the end of this parliament, alongside their other priorities for housing, this should give consumers the certainty they need to determine if they will relocate or not.

“Should inflation also continue to drop, the Bank of England may feel confident to start cutting interest rates to provide the housing market with a much-deserved summertime boost.”

5 July: All Eyes On Labour Government’s Housing Policy

- House prices fall 0.2% in June

- Average values up 1.6% year-on-year

- Average property price £288,455

House prices fell marginally last month by 0.2% (less than £500 in cash terms), taking the annual rate of price inflation in the year to June to 1.6%, according to the latest figures from mortgage lender Halifax.

The annual rate of change is the same as that recorded in May, showing price change is largely flat. This has been the case for three consecutive months, as buyers have continued to face high mortgage costs. A typical home now costs £288,455 (compared to £288,931 in May).

Northern Ireland has recorded the strongest property price growth of any nation or region in the UK, rising by 4.0% in the year to June, up from 3.3% the previous month. The average price of a property in the country is now £192,457.

In England, the steepest rate of house price inflation is in the North West region, up by 3.8% over the last year. Average prices are now at £231,351.

House prices in Scotland increased by 1.6% annually, with a typical property now costing £204,663, and in Wales house prices have posted annual growth of 2.7% to reach an average of £220,197.

Eastern England is the only region to register a decline in house prices over the last year, down by 0.9%. The average home here is worth £328,747.

London continues to have the most expensive property prices in the UK, now averaging £536,306. Property prices in the capital are up by 0.9% compared to last year.

Alice Haine, an analyst at Bestinvest, said: “With the country waking up to a Labour government, many may wonder whether the landslide victory will inject some momentum into the property market.

“A stable political environment can potentially deliver a confidence boost to the housing market, particularly one that has struggled over the past year with high borrowing costs and a dearth of available and affordable stock.

“Interest rates have remained at a 16-year high of 5.25% for almost a year causing major affordability challenges for first-time buyers and those looking to move to larger homes. While the combination of lower inflation and strong wage growth has offered a slight boost to affordability, for many the dream of home ownership is still out of reach.”

The Bank of England will reveal its next Bank Rate decision on 1 August.

Myles Moloney at estate agent Chase Buchanan said: “June’s property market remained positive and house hunters with larger equity and buying power pushed on to agree a sale as they felt the result of the election was a foregone conclusion.

“Buyers who are only just starting their property search, however, have been slightly more cautious to observe how the manifestos could benefit them during their property buying journey – particularly first-time buyers.”

1 July: Values Rise 0.2% As Interest Rate Cut Hangs In Balance

- House prices edged up 0.2% in June

- Values are 1.5% higher than a year ago

- The average property is worth £266,604

The latest data from Nationwide building society showed house prices nudged up just 0.2% in June, writes Jo Thornill. This pushes the annual rate of inflation to 1.5%, compared to 1.3% in May.

It means the average UK home is now worth £266,604 – just 3% below the all-time high recorded in the summer of 2022.

However, the mutual lender’s data shows that housing market activity has been broadly flat over the past 12 months, and is 15% lower compared to 2019 levels.

Transactions involving a mortgage are down even further (nearly 25%), reflecting the impact of higher borrowing costs. By contrast, the volume of cash transactions is around 5% higher than pre-pandemic levels.

There remains stark differences between house prices across the regions. While some areas, predominantly Northern Ireland and some areas in the north of England, have seen a modest pick up in growth, others, mainly in the South and the East of England, are still recording annual price declines.

The regions with the biggest growth were Northern Ireland and the North West, which both saw annual price rises of 4.1% at the end of the second quarter of 2024. Average prices in the regions stand at £190,300 and £213,580 respectively. See below graph.

East Anglia experienced the biggest annual fall with a drop of 1.8% in the same period. Average property values in the region are £270,597.

Prices in London are up 1.6% for the year to the end of Q2. Prices in the capital remain the highest of any region at an average of £525,248.

Robert Gardner, Nationwide’s chief economist, said: “While earnings growth has been much stronger than house price growth in recent years, this hasn’t been enough to offset the impact of higher mortgage rates, which are still well above the record lows prevailing in 2021 in the wake of the pandemic. Housing affordability is still stretched.

“Today, a borrower earning the average income buying a typical first-time buyer property with a 20% deposit would have a monthly mortgage payment equivalent to 37% of take-home pay – well above the long term average of 30%.”

Mark Harris, chief executive of mortgage broker SPF Private Clients, said: “With inflation hitting the Bank of England’’s 2% target, we are edging ever closer to that first rate cut, perhaps as soon as next month. After years of rising rates, followed by months of rate holds, that first reduction, when it comes, will send an important message to borrowers, enabling them to plan their moves with more confidence.

“That said, borrowers will still have to get used to paying more for their mortgages, with the days of rock-bottom rates long gone.”

28 June: Values Expected To Increase By Year End

- Prices flatline in May

- Sales agreed 8% up on last year

- Prices estimated to be 8% over-valued

- Average property price at £264,300

House prices were flat in May, according to the figures from property website Zoopla, but values are on track to be around 1.5% higher (£3,900 in real terms) by the end of the year, writes Jo Thornhill.

Zoopla says buyers and sellers have not been put off by the general election campaign, with a fifth more homes (19%) on the market this month compared to the same period last year.

In addition, demand for properties for sale is up by 6% while sales agreed are up 8%, year on year.

Zoopla uses wages data and mortgage rates to assess whether property values are fair. It estimates house prices are around 8% over-valued due to the big jump in mortgage rates in 2023.

However, it says this over-valuation should disappear by the end of the year, assuming house prices rise by around 1.5%, mortgage rates remain at an average of 4.5%, and rising incomes and longer mortgage terms help to improve affordability.

There are signs that market activity is beginning to slow, as tends to be the trend in the summer months. Sales agreed are down month on month across all regions, with the biggest falls in the North East (down 6% in May) and the West Midlands (down 5%).

The overall stock of homes for sale has grown gradually across all regions, although at a slower pace than earlier in the year.

Richard Donnell, executive director at Zoopla said: “The housing market continues to adjust to higher borrowing costs through modest house price falls and rising incomes. Buyers using mortgages are also relying on longer terms to gain that extra few percentage points of buying power to afford a home.

“The general election campaign has had a limited impact on market activity although the seasonal summer slowdown is arriving. Sales agreed continued to increase and more homes for sale means more buyers looking to move in the second half of the year. The timing of the first cut in the base rate [by the Bank of England] is a key moment and will give a boost to both market sentiment and sales activity. Overall we expect house prices to be 1.5% higher over 2024.”

Guy Gittins, chief executive of estate agent Foxtons, said: “While house price inflation is flat, we’ve seen consistently positive demand and sales agreed activity this year. With forecast house price rises now roughly in line with current inflation rates, it’s clear property ownership is still high on the agenda for hundreds of thousands of people across the UK.”

Myles Moloney, sales manager at estate agency Chase Buchanan, said: “June’s property market to date has remained positive and house hunters with larger equity and buying power have pushed on to agree a sale as they feel the result of the election is foregone.

“Buyers who are only just starting their property search, however, have been slightly more cautious to observe how the manifestos could benefit them during their property buying journey – particularly first-time buyers.”

HM Revenue & Customs figures out today show a modest recovery in housing market activity with residential transactions for May up by 17% to 91,290, compared to May 2023.

It is the fifth consecutive month-on-month increase, rising 2% from the 89,160 transactions recorded for April 2024.

Amy Reynolds, head of sales at estate agency Antony Roberts in Richmond, south west London, says: “Although transaction numbers have edged up, this masks regional fluctuations with localised economic factors such as employment growth or new infrastructure projects coming into play.

“While inflation appears to be where the Government wants it, high debt levels and rising interest rates for many will lead to ongoing reduced spending power in other areas of the economy. Reducing interest rates may help homeowners with mortgages, but it doesn’t help the rest of the population. We are speaking to more people who are looking to downsize to release capital to live on and that is hugely concerning.”

19 June: Market Expects Interest Rate Cut In August

- House prices up 1.1% in year to April

- Second month of annual price rises

- Average house price £281,000

Average UK house prices increased by 1.1% in the year to April 2024, according to data from the Office for National Statistics (ONS). This is up from the 0.9% annual rise recorded in the year to March, writes Jo Thornhill.

It is the second consecutive month to record an annual increase in average prices following eight months of annual falls, suggesting stability could be returning to the market.

Today’s news on inflation falling to its target of 2% is likely to lead to an interest rate cut by the Bank of England, with experts predicting it will be in August. This would feed through to mortgage rates, which would further boost the housing market.